Auto logout in seconds.

Continue Logout

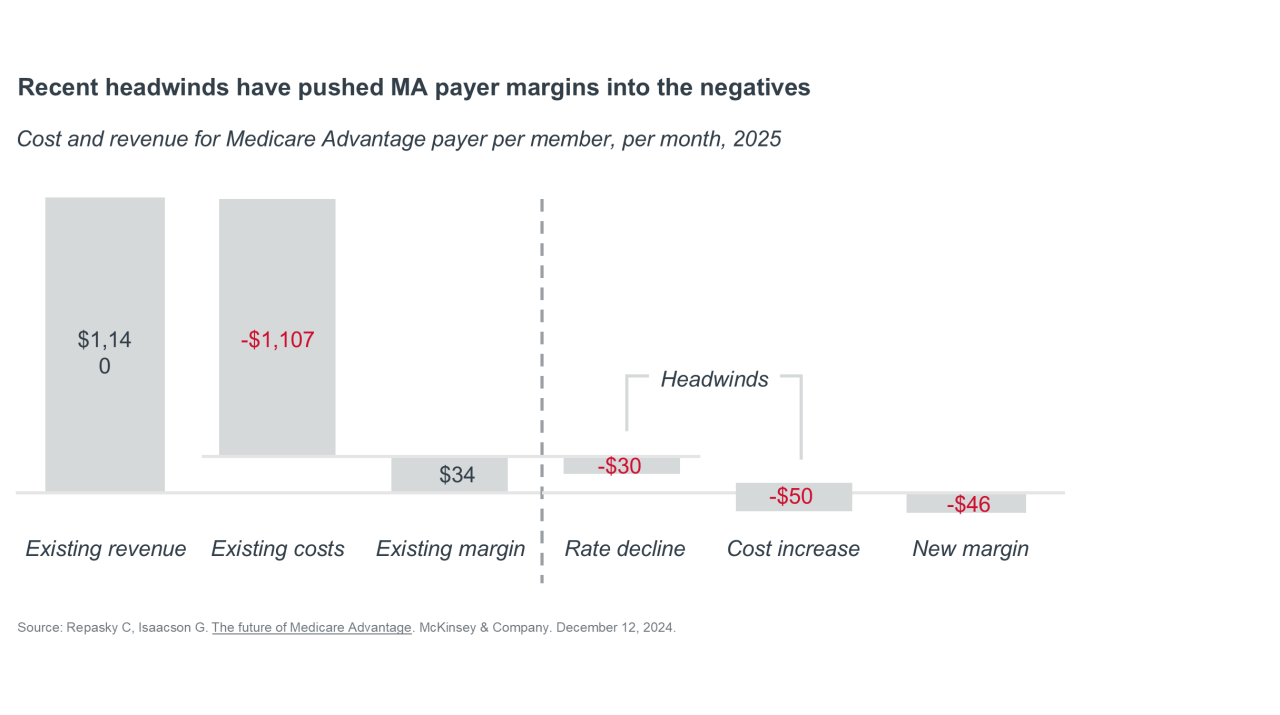

The Medicare Advantage landscape is currently defined by rising care utilization among seniors and increasing regulatory oversight from CMS. These factors lead to increased medical costs and lower than expected payments for Medicare Advantage (MA) plans, pushing MA payer margins into negative territory and forcing insurers to make difficult choices about product design, benefit offerings, or (at the most extreme end of the spectrum) their participation in the MA market entirely.

Understanding the factors straining MA plan finances

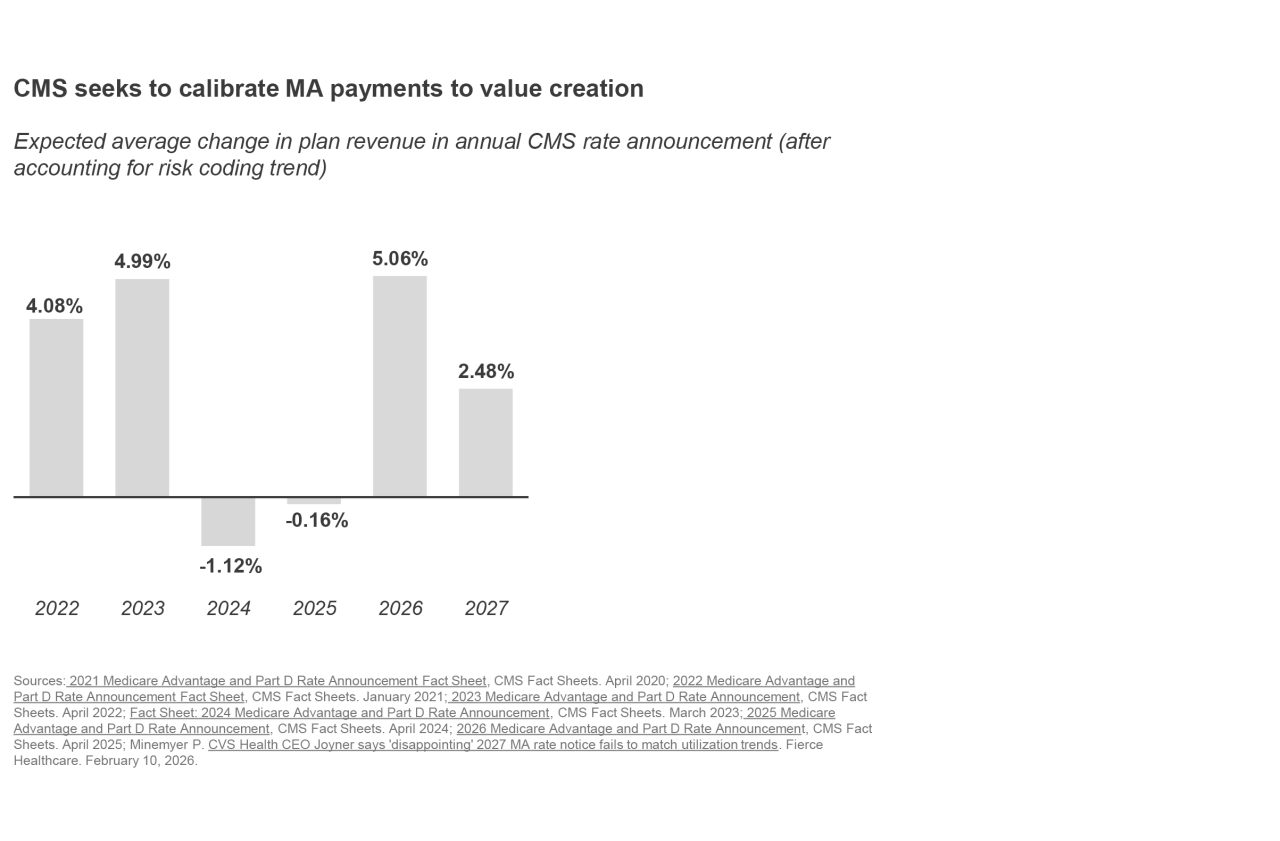

Following years of favorable finances, 2024 and 2025 saw health plans absorb payment rate cuts in consecutive years.

At Advisory Board, we’ve referred to this as the “era of austerity” for Medicare Advantage plans. And while 2026 saw a more favorable rate increase of roughly 5% (reflecting rising utilization among the MA population), CMS has proposed maintaining roughly flat rates in their 2027 Advance Notice.

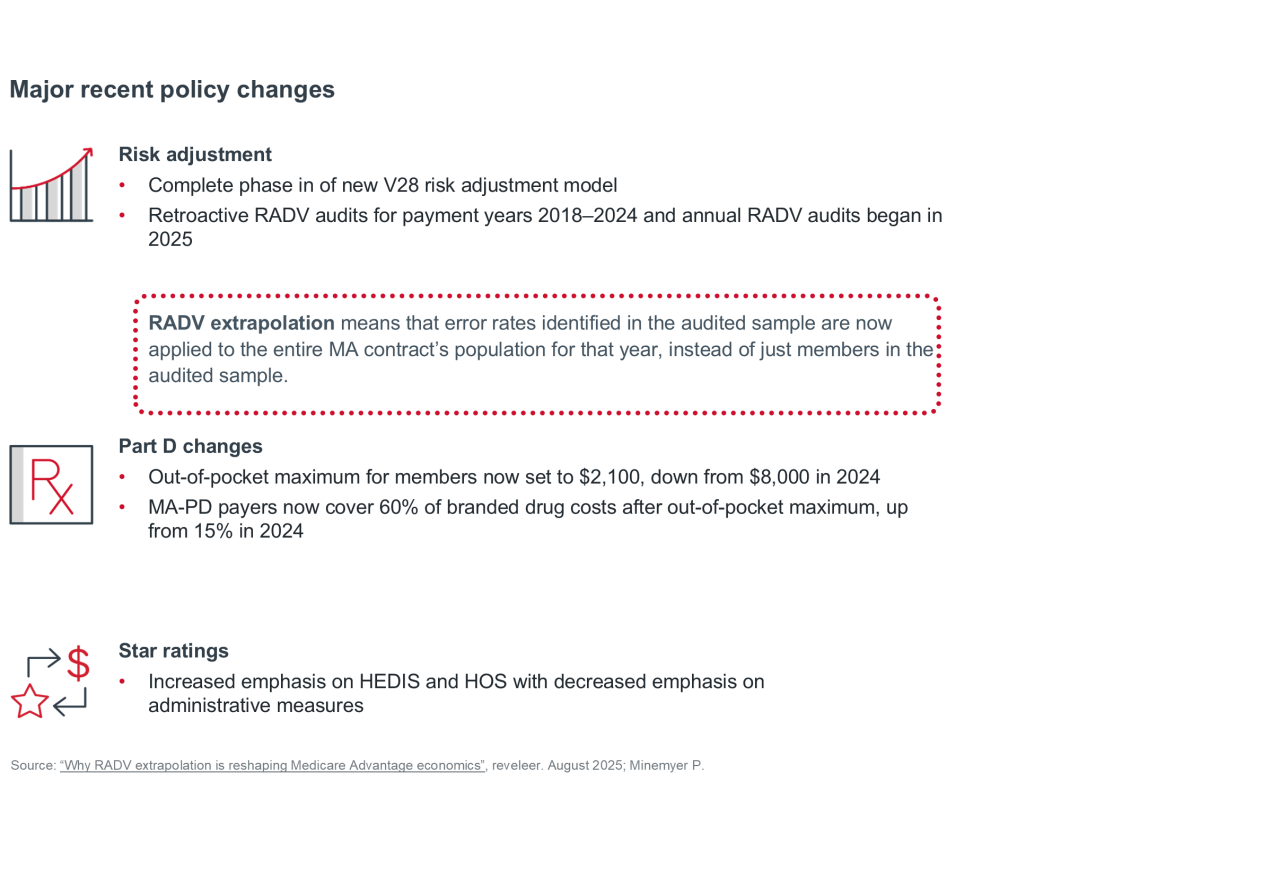

This financial pressure has been magnified by several overlapping policy shifts, including the complete phase in of the V28 risk adjustment model, which is meant to push Medicare Advantage organizations (MAOs) to produce more granular documentation and coding of MA patients, and major retroactive Risk Adjustment Data Validation (RADV) audits that aim to “claw back” overpayments to risk-bearing entities stemming from inaccurate coding practices.

Simultaneously, CMS has implemented tougher Star rating methodology that increases emphasis on Healthcare Effectiveness Data and Information Set (HEDIS) and Health Outcomes Survey (HOS) measures while decreasing emphasis on administrative functions. These tweaks clearly point to CMS’s interest in seeing more managed care success (i.e., better clinical outcomes at reduced cost to the government). As a result, achieving a Star rating of five has become increasingly difficult for plans, making it an even greater differentiator in terms of plan success moving forward because of the substantial bonus dollars tied to higher ratings.

In parallel, substantive Part D redesign now caps out-of-pocket drug spend for members at $2,100, shifting the financial responsibility of drug costs away from seniors and onto plans and manufacturers.

"The proposed rate simply does not match the level of medical cost trend in the industry."

CEO of a national health plan

Underlying these regulatory dynamics, Medicare Advantage plans have also struggled to manage clinical costs amid rising utilization among seniors — leading to consistently elevated medical loss ratios (MLRs). While reported MLRs vary based on each organization’s broader business mix across MA and other lines of business, large national payers have generally reported MLRs in the high-80% to low-90% range.1

While these utilization dynamics are hitting home now, the future may prove even more challenging. By 2032, the majority of Medicare Advantage beneficiaries will be 75 or older.2 As seniors continue aging, chronic disease prevalence is also rising. Hypertension, high cholesterol, and arthritis have consistently ranked among the top ten most common conditions since 2015, but prevalence has surged, with arthritis alone growing from affecting 31% of adults a decade ago to 51% in 2025. These dynamics portend a future where managing specialist spend will be a critical priority for MA plans.

How Medicare Advantage plans are responding

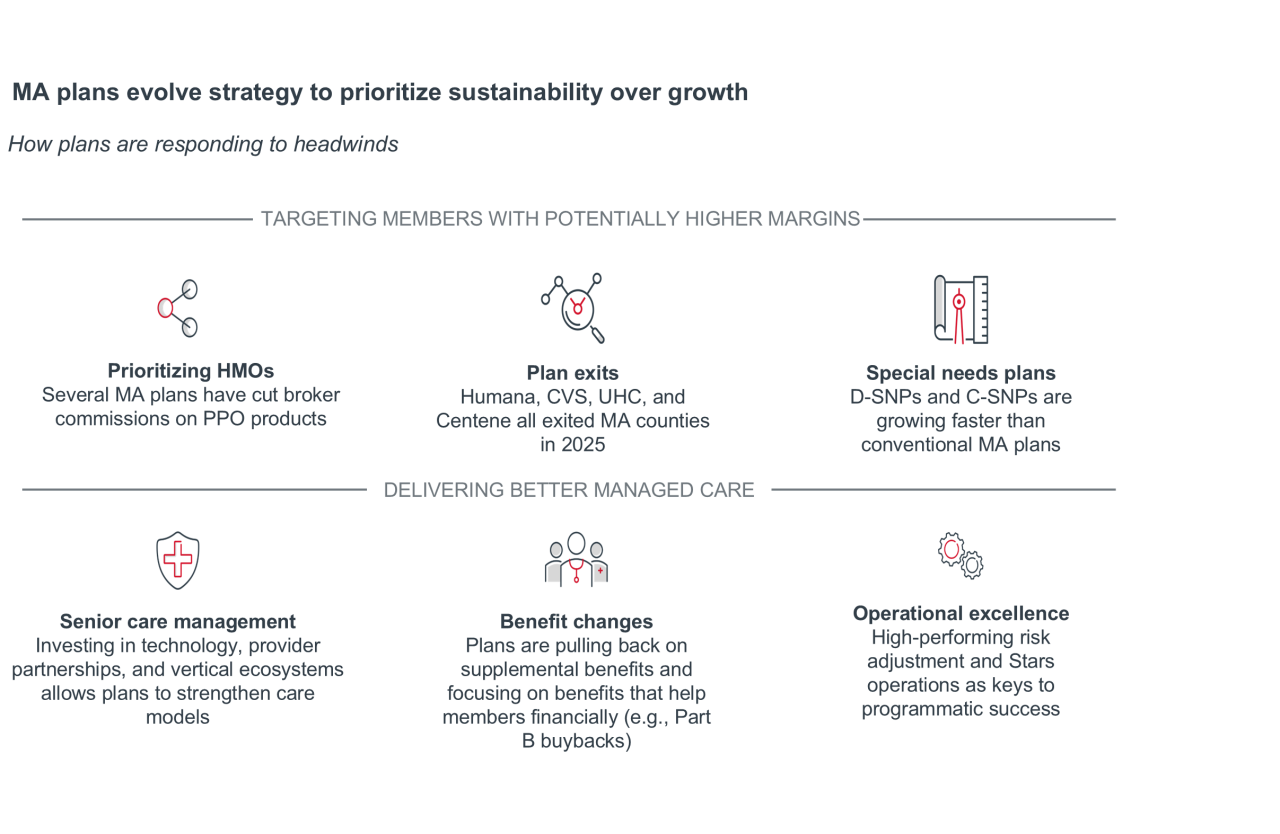

Plans have responded to this constrained financial environment by shifting from a “growth at all costs” mindset to a focus on restoring sustainable margins.

The first step MA plans are taking to rightsize margins is targeting potentially higher-margin members for enrollment — prioritizing HMO products, exiting less desirable markets, and focusing on special needs plan (SNP) growth. The second step is delivering better managed care through benefit changes, reinvigorated senior care management efforts, and a recommitment to MA fundamentals (e.g., risk adjustment, Stars performance, quality improvement programs).

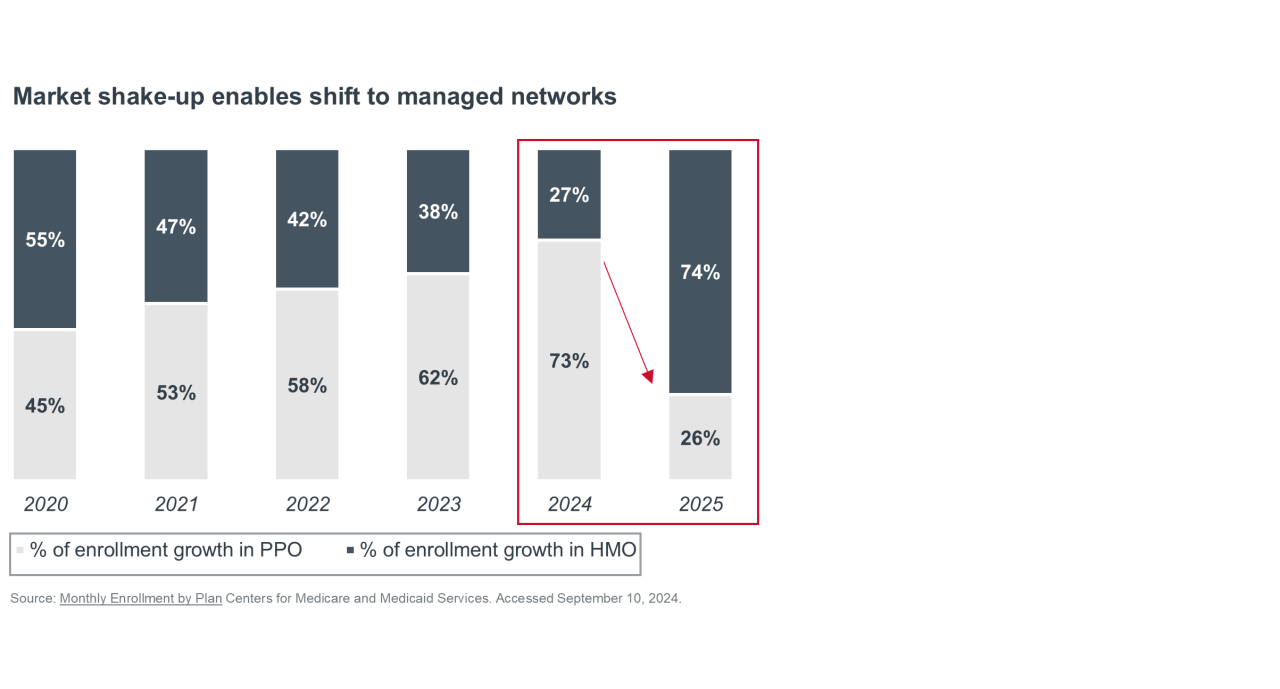

MA plans are targeting potentially higher-margin members.

Preferred provider organization (PPO) plan enrollment has seen consistent growth for over a decade because seniors prefer the flexibility of larger provider networks. And, during more favorable financial times, MA plans leveraged that appeal as a means of growing enrollment. However, rising care costs and an older, sicker membership have made PPOs less viable for MAOs. In response, plans have adjusted strategies — such as altering broker commissions — to encourage HMO enrollment.

Beyond the individual MA market, plans are actively pursuing SNP enrollment as a means of profitable growth. In the 2025 annual enrollment period, half of all new MA enrollees came in through a SNP, reflecting how these plans have shifted from niche products to a core growth engine. SNPs generate higher rebate dollars per member than other MA plan types, enabling plans to offer richer benefits and boosting enrollment. While dual-eligible SNPs (D-SNPs) have consistently seen growth for several years, chronic condition special needs plans (C-SNPs) have become the fastest growing SNP type most recently, jumping from just 1 in 200 new MA enrollees in 2022 to 1 in 3 by 2025.3

MA plans are trying to deliver better managed care.

Beyond new growth lanes, MA plans are pulling levers to rightsize finances and focus on their core managed care efforts. The most notable example relates to the richness of supplemental benefits like fitness, transportation, and meal benefits. Plans are pulling back on nice-to-have benefits and increasing benefits that support member finances directly like Part B buybacks, while maintaining core supplemental benefits such as dental and vision.

Simultaneously, plans are adapting to the Inflation Reduction Act’s redesign of Part D by increasing Part D deductibles. The average Part D deductible jumped from $63 in 2024 to $225 in 2025, coinsurance prevalence rose from 11% to 57%, and 45% of members who had no deductible in 2024 have one in 2025.

High-performing regional plans are pursuing better managed care through stronger provider partnerships that strengthen senior care management, and delivering unique products focused on social services. Some examples include Sanford Health integrating clinicians and therapists into the primary care setting, Clover Health Clover using AI-driven physician decision support to reduce hospitalization, Devoted Health’s in-house virtual diabetes program, which reduced average HbA1c by 2.4 points in 100 days, and Alignment Healthcare’s virtual application tech platform, which uses AI clinical stratification to fill gaps in care coordination.4

While national MA plans will also pursue the strategies above, they also leveraged their scale and capital to diversify into adjacent care delivery services, notably primary care, home health, pharmacy, and behavioral health. By owning and integrating these end-to-end services within a single ecosystem, plans hope to coordinate care more effectively and better manage utilization. While recent MLR challenges for national plans indicate they have yet to fully realize the benefits of these ecosystems, the potential remains for improved patient management through an integrated finance and delivery system.

Lastly, the recent “era of austerity in Medicare Advantage” has been a reminder to MAOs about the importance of operational excellence, particularly related to risk adjustment and Stars — including the importance of identifying synergies that support multiple goals. MA plans are evaluating AI technologies as a tool to identify high-risk members earlier, close care gaps, and drive members to complete health risk assessments (HRAs).

A path forward for MA

MA is being pushed back to its roots, and it is a program intended to incentivize plans to deliver innovative, cost-effective care for a population that is not always easy to manage. Recent federal changes, particularly adjustments in Star ratings incentives and benchmarking methodologies, signal a push for private payers to return to fundamentals of managed care. To address the question of whether health plans can turn their MA business around, they will need to deliver stronger, more efficient managed care.

1 Tepper, N. Humana borrows UnitedHealth’s Medicare Advantage playbook. Modern Healthcare. August 25, 2025; Molina Healthcare Reports Second Quarter 2025 Financial Results. Molina Healthcare Inc. July 23, 2025; Elevance Health Reports Second Quarter 2025 Results. Elevance Health. July 17, 2025; CVS Health Corporation Reports Second Quarter 2025 Results and Updates Full-Year 2025 Guidance. CVS Health Corporation. July 31, 2025; CMS Ramps Up RADV Audit Plans, But Questions Remain About Process. AIS Health. June 5, 2025; Molina Healthcare subsidiaries & acquisitions. Greyb Insights. June 13, 2024.

2 Howden L, Meyer J. Age and Sex Composition: 2010; Census.gov. 2023 National Population Projections Datasets.

3 Advisory Board analysis of Monthly contract and enrollment summary report, CMS, July 2016-2025. Trends in C-SNP Enrollment and Offerings, 2018-2025. ATI Advisory. September 3, 2025; Tepper N, Eastabrook D. Insurers, in-home providers chase C-SNP Medicare Advantage Market. Modern Healthcare. March 20, 2025; Freed S, et al. 10 Things to Know About Medicare Advantage Dual-Eligible Special Needs Plans (D-SNPs). KFF. February 9, 2024; Freed M, et al. Medicare Advantage in 2024: Enrollment Update and Key Trends. KFF. August 8, 2024; Friedman J, et al. Medicare Advantage industry: Dual-eligible plan valuation and selected benefit offerings. Milliman. December 19, 2024.

4 Heinert P. Sanford report details pledge to patients, communities. Sanford Health News. June 6, 2024; Devoted Health Raises New Funding to Deliver On Its Mission to Improve the Health and Well-Being of Older Americans. Devoted Health. December 29, 2023; Morse S. Clover Health is offering its AI assistant to all Medicare Advantage payers and providers. Healthcare Finance News. May 30, 2024; Diamond F. Alignment Health rolls out MA plans with enhance food benefits. Fierce Healthcare. October 3, 2023; Landi H. Alignment Healthcare grows Q3 revenue to $994M, boosts 2025 outlook, Fierce Healthcare. Oct 31, 2025.

Posted on May 13, 2026

Don't miss out on the latest Advisory Board insights

Create your free account to access 1 resource, including the latest research and webinars.

Want access without creating an account?

You have 1 free members-only resource remaining this month.

1 free members-only resources remaining

1 free members-only resources remaining

You've reached your limit of free insights

Become a member to access all of Advisory Board's resources, events, and experts

Never miss out on the latest innovative health care content tailored to you.

Benefits include:

Unlimited access to research and resources

Member-only access to events and trainings

Expert-led consultation and facilitation

The latest content delivered to your inbox

You've reached your limit of free insights

Become a member to access all of Advisory Board's resources, events, and experts

Never miss out on the latest innovative health care content tailored to you.

Benefits include:

Unlimited access to research and resources

Member-only access to events and trainings

Expert-led consultation and facilitation

The latest content delivered to your inbox

This content is available through your Curated Research partnership with Advisory Board. Click on ‘view this resource’ to read the full piece

Email ask@advisory.com to learn more

Click on ‘Become a Member’ to learn about the benefits of a Full-Access partnership with Advisory Board

Never miss out on the latest innovative health care content tailored to you.

Benefits Include:

Unlimited access to research and resources

Member-only access to events and trainings

Expert-led consultation and facilitation

The latest content delivered to your inbox

This is for members only. Learn more.

Click on ‘Become a Member’ to learn about the benefits of a Full-Access partnership with Advisory Board

Never miss out on the latest innovative health care content tailored to you.

Benefits Include:

Unlimited access to research and resources

Member-only access to events and trainings

Expert-led consultation and facilitation

The latest content delivered to your inbox